Blog

Blog

Últimos mensajes

Temas mas recientes

|

Esta sección te permite ver todos los posts escritos por este usuario. Ten en cuenta que sólo puedes ver los posts escritos en zonas a las que tienes acceso en este momento.

Mensajes - senslev

1

« en: Hoy a las 13:07:20 »

Cero certidumbre en bolsa, si fuese así, no podría ser.

A no ser que te refieras a que está todo amañado, entonces, para los que lo controlan sí que hay certidumbre, para el resto es todo una ilusión y de ahí la transferencia de riqueza de la mayoría a esos que lo controlan todo (en teoría certidumbre a lo largo del tiempo, no a corto plazo, por lo que volvemos a lo de que no hay certidumbre).

O igual no se a qué te refieres, que también puede ser.

2

« en: Hoy a las 12:41:40 »

Por definición certidumbre y bolsa son dos términos incompatibles. En la vida también. Claro, senslev... pero es que el problema es otro.

Quieren certidumbre. ¿Para qué? Para posicionarse en Bolsa. Tú futuro, tu bienestar les importa un carajo. Quieren imponer algo, y les da igual qué... Sólo quieren apostar a caballo ganador.

Entonces: Bolsa, ni tocar. Medidas consensuadas y razonables. Ciencia, toda la que se pueda. Paciencia. (Y barajar, je, je.)

4

« en: Hoy a las 11:55:10 »

Ya he puesto diversas fuentes que tratan sobre el cambio climático. Las vuelvo a poner. Los datos, la interpretación de los datos y la honradez de quien los interpreta, asumiendo el conocimiento correspondiente, ya no es mi problema. Esto es como la inflación, según ppcc no hay inflación o es inflación falsa, bueno, pues mi percepción es otra. ¿Hace más calor que antes y el clima ha cambiado?, sí, esa es mi percepción, ¿comparándolo con qué?, pues con el tiempo que llevo vivo básicamente. https://www.rankia.com/blog/game-overEjemplo de la AMOC: https://www.rankia.com/blog/game-over/6253442-manipulacion-mediante-mala-ciencia-ficcion-climaticahttps://www.youtube.com/@thegreatsimplification/featuredhttps://dothemath.ucsd.edu/https://escholarship.org/uc/energy_ambitions

5

« en: Hoy a las 11:32:17 »

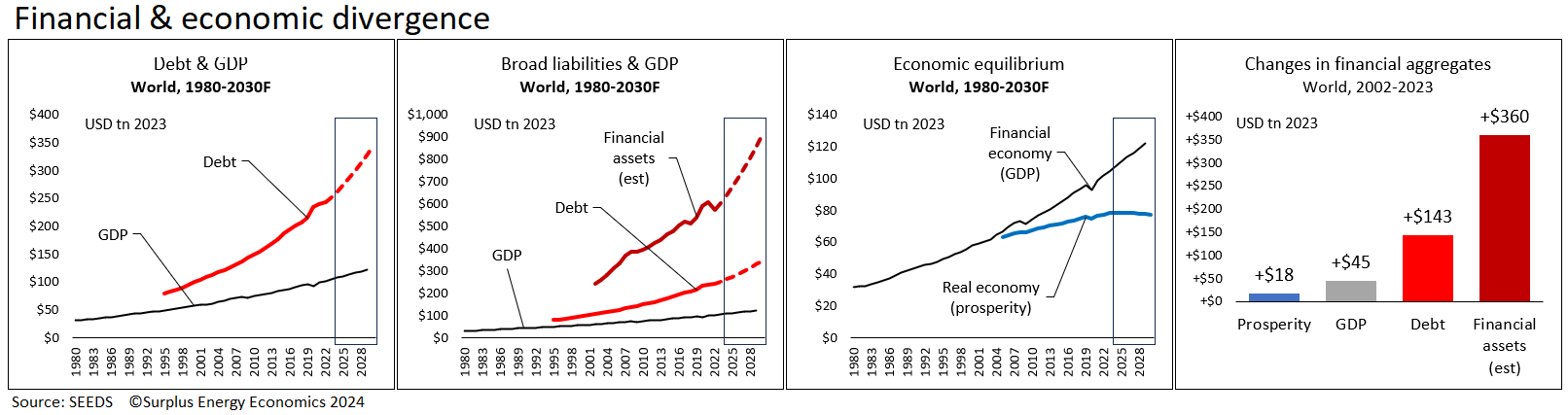

https://surplusenergyeconomics.wordpress.com/2024/05/07/277-at-the-limits-of-monetary-possibility/#277: At the limits of monetary possibility

Posted on May 7, 2024

HOW DOES THIS END?

On two occasions in modern times, central banks have found themselves obligated to pour huge amounts of newly-created money into the system. The first instance was the global financial crisis of 2008-09, and the second was the coronavirus pandemic of 2020-21.

Neither of these events was anticipated, though the first one certainly should have been. You would have to be very brave indeed to bet against another out-of-the-blue shock forcing central bankers back into flooding the economy with liquidity.

In fact, the very structure of the financial system makes a future shock inescapable. Over the past twenty years, and depending on the definitions used, each dollar of growth in the global economy has been accompanied by between $3 and $8 of newly-created financial liabilities.

Simply stated, the financial system has been allowed to grow far more rapidly than the underlying economy itself, and this creates a wholly unsustainable set of trends which will lead to a drastic reset of the relationship between the economy and the financial system.

This has happened because we’ve been trying to counter, whilst at the same time denying, structural deterioration in the global economy. Driven by the depletion of oil, natural gas and coal resources, the material costs of energy have been rising relentlessly, and, contrary to widespread assurances, renewables cannot provide a new source of abundant low-cost energy to the economy.

In essence, we’ve been trying to overcome material economic deceleration with monetary stimulus, a technique that cannot work, but for which no alternative exists.

As you may know, we have a limitless capability for the creation of money, but the banking system can’t lend energy or other natural resources into existence, and central banks cannot conjure them out of the ether.

Building the next crisis

The main driver of super-rapid monetary expansion hasn’t been central bank money-creation. Rather, the central banks have acted as the last line of defence when credit excess, generated elsewhere, has threatened to fracture the system.

Not later than 2007, the global credit mountain had reached a scale at which it could no longer be serviced at normal rates of interest. The purpose of subsequent rate-slashing, reinforced by QE, was to prevent the servicing of this credit mountain from becoming completely unaffordable.

But making credit cheap to service also means making it cheap to obtain. We need, but have yet to find, new tools for managing the supply of credit to the economy in ways that do not exacerbate systemic risk.

As the world’s stock of credit has grown, the system has simultaneously become both more complex and more dangerously inter-connected.

In the modern economy, in which most money is loaned into existence, each unit of money is tied to a corresponding obligation. Accordingly, whenever we try to use credit expansion to stimulate the flow of activity in the economy, we simultaneously add to the stock of financial commitments.

Meanwhile, tightening the regulation of conventional banks has pushed ever more of the process of credit expansion into the unregulated, and higher-risk, “shadow banking” (NBFI) system, where even quantitative data is neither complete nor timely.

The next financial crisis is likely to originate in some esoteric part of the system that most members of the public have never even heard of. When this happens, the current policy of countering inflation by raising rates, and reversing QE into QT, will, by force of necessity, have to be thrown into reverse.

We’ve always known that the unanchored fiat money system creates a temptation for the authorities to resort to excess money-creation, thereby undermining the purchasing power of money.

Less thought seems to have been devoted to the possibility, which has now become a probability, of them being compelled to expand the stock of money by failure somewhere within the top-heavy, super-complex, dangerously interconnected and excessively-stressed financial system itself.

Hitting the panic-button

Both the 2008-09 and the 2020-21 interventions were inflationary, as the creation of new central bank money always is. The difference, though, was the point at which this inflation showed up.

During and after the GFC, the inflationary effects of QE were largely confined to capital markets, creating the “everything bubble” in asset prices. During the pandemic, however, newly-created money was channelled, via enormous government deficits, into the broader economy of households and businesses.

By convention, soaring asset prices aren’t included in headline definitions of inflation, and it was only when QE largesse was redirected to households that measured consumer price inflation took off. This taught everyone something that many had understood all along, which is that, notwithstanding routine assurances to the contrary, central bank money creation is inherently inflationary.

Our attitudes to these differing forms of inflation are inconsistent. When asset prices soar, the (generally older) owners of assets rejoice at the increase in their paper wealth, whilst scant attention is paid to the plight of younger people, whose aspirations to acquire homes and other assets get priced ever further out of their reach.

When consumer price inflation takes off, on the other hand, households experience hardship, voters get angry, and officialdom sits up and takes notice.

This is why, since 2021, most central banks – with the noteworthy exception of the Bank of Japan – have adopted counter-inflationary, restrictive monetary policies, implemented by raising policy interest rates, and by reversing QE into QT.

This plan hasn’t yet faced a serious challenge. The collapse of SVB was a minor event, whilst the Truss-Kwarteng mini-budget was just a little local idiocy – but both set the hands of central bankers quivering over the QE-button.

In one sense, though, the Truss-Kwarteng fiasco was instructive – the Bank of England wasn’t forced to intervene by a falling currency alone, or by surging gilts yields, but by the implications for another part of the system, which, in this instance, was pension funds made vulnerable by the use of LDI (liabilities-driven investment), with its dependency on gilts prices as collateral. We could call this a ‘second-hand’, ‘second-order’ or unintended consequences type of risk.

This is a prime example of complexity risk in the sprawling, interconnected system of global credit.

The theory of restrictive monetary policy is that inflation can be brought back under control by cooling the rate of borrowing. One of the attendant risks is that raising the cost of capital could trigger a market crash by puncturing the “everything bubble”, which was created through the provision of vast amounts of recklessly cheap capital. Another is that these policies might simply fail to bring headline inflation under control.

What we are waiting for – whether we acknowledge this or not – is the next really big test of central bankers’ resolve. We don’t, and probably can’t, know exactly where this will come from – but we do know that it will.

Found in translation

Through these various gyrations, monetary policy has become the only game in town. Where investors, analysts and commentators once concentrated on a host of issues as diverse as OPEC oil price intentions, political or geopolitical stresses, trade balances or the direction of economic activity, the debate has shifted to the new centre-ground of interest rate forecasting.

This, as Ann Pettifor has said, “is tricky terrain for economists, because – remarkably enough – they are not routinely trained in the theory of money and banking. You can get through an economics degree, even an economics career, without pausing to think seriously about either”.

“To understand how grave an intellectual vacuum this leaves”, she continued, “imagine the chaos if physicists working on space projects had not been trained in the theory of gravity – a concept that is fundamental to physics in the way that money is fundamental to the economy”.

This isn’t territory onto which any non-specialist should lightly venture. But Surplus Energy Economics uses a concept which we can claim to be unique, and which can add value to the debate.

This is the concept of two economies. Instead of referencing “the” economy, and interpreting it entirely in monetary terms, we recognise that the “financial economy” of money, transactions and credit exists in parallel with the “real economy” of material products and services.

This understanding enables us to recognize that inflation, and numerous other economic processes, are functions of changes in the relationship between the monetary and the material economies.

From this perspective, we can define prices as “the monetary values ascribed to material products and services”. We can go on to state that “money has no intrinsic worth, but commands value only as an exercisable claim on the output of the “real” or material economy”.

Effective interpretation, then, requires the conjoined analysis of the monetary and the material.

Each of these two economies has its own identifiable processes. The real economy operates by using energy to convert raw materials into products. (This definition also embraces services, because no service can be provided without physical artefacts, and there is no such thing as an ‘immaterial economy’).

The critical processes in the financial economy are the creation, deployment and elimination of money as credit, and the interplay between the flow and stock of money in the system.

We need to be aware that the monetary and the material economies have an in-built tendency towards equilibrium, because the value of money exists only as a claim on the material. If, put at its very simplest, we double the flow of money in the system, but are unable to increase the size of the material economy, then the rate of exchange between the two must halve, to bring them back into balance.

In short, if we create excess claims in the system, these excesses must be eliminated in a process that can be thought of as value destruction. This occurs either through formal default or through the informal or soft default of monetary devaluation through inflation.

The dynamics of self-delusion

What, then, has actually been happening to the “two economies” in the comparatively recent past?

The answer, simply stated, is in three parts.

First, material prosperity has carried on growing, though the rate of increase has slowed to a microscopically small amount.

Second, the flow of monetary activity measured as GDP has grown at a higher and seemingly-satisfactory rate.

Third, though, the stock of financial commitments – the aggregate of debts and quasi-debts – has soared, drastically out-pacing the economy itself.

We can quantify these trends, with all data used here stated at constant 2023 values, in dollars converted from other currencies at market exchange rates.

Since 2002, global debt has increased by $143tn, or 130%. But broader financial assets – which are the liabilities of the government, household and private non-financial corporate (PNFC) sectors of the economy – have grown by about 150%, or $360tn, over that same period.

This latter number can only be an estimate, because some jurisdictions choose not to report financial assets data to the Financial Stability Board. The FSB is a monitoring organisation, not a regulatory one. The estimates cited here are likely to be understatements because, whilst most sizeable economies are included in the FSB data series which start in 2002, only two of the world’s specialised, hugely-leveraged financial centres – Luxembourg and the Cayman Islands – supply data to the FSB.

Over that same period, global real GDP expanded by $45tn, or 74%. This means that each dollar of reported growth between 2002 and 2023 was accompanied by $3.20 of net new debt, or by about $8 of net new broad financial assets.

The resulting trajectories are unsustainable, as the accompanying charts illustrate – debt is fast out-pacing GDP, broader liabilities are in turn out-growing both debt and GDP, whilst material prosperity is far adrift even of financial flow, let alone of monetary stock,

Moreover, the stock and flow data series aren’t really discrete, since credit expansion results in an increase in the aggregate of financial transactions which are measured as GDP.

Put another way, we are lending money into existence, and then counting the spending of that newly-created credit as “activity” for the purposes of measuring the size of the economy, whilst ignoring questions about the servicing or repayment of debt.

On this basis, we’re entitled to conclude that we’ve been manufacturing “growth” through the breakneck expansion of credit, and that this “growth” could only be regarded as genuine if we assumed that debt and broader liabilities need never to be honoured.

If it takes somewhere between $3 and $8 of new debt or quasi-debt to generate a dollar of GDP growth, paying off debt incurred in the present from growth generated in the future is a mathematical impossibility.

An example here is the United States which, during 2023, generated reported real growth of $675bn on the back of a $2.4tn fiscal deficit.

America, of course, is in a privileged position, able to borrow readily from other countries because of the reserve status of the dollar, and the use of USD in energy and other critically-important commodity markets.

Even the US, though, can hardly carry on adding government debt at a rate of $1 trillion every hundred days before the markets, and the public, start to ask hard questions about the real character of economic “growth”, and recognise that – whether in America or elsewhere – our growing mountains of debt and quasi-debt can never be honoured ‘for value’ from the proceeds of “growth”.

To tie these various numbers to underlying reality, SEEDS calculates that global material economic prosperity increased by less than 8% between 2002 and 2023, a period in which aggregate liabilities expanded by close to 170%, and non-government liabilities by an estimated 180%.

These numbers look a bit better in PPP- rather than market-converted terms, because the purchasing-power parity FX convention attaches proportionately greater weight to economies such as China, India and Russia.

But the fact remains that credit expansion is driving reported growth at rates which, whilst they far exceed underlying material reality, can never catch up with the rates at which debt and quasi-debt are growing. SEEDS undertakes these calculations by backing out the inflationary credit-effect element in GDP growth, and deducting the all-important Energy Cost of Energy, or ECoE, from the resulting calculation of underlying or ‘clean’ economic output.

We could, at some later date, explore the process of credit creation within the regulated banking and the unregulated “shadow banking” (NBFI) sectors. But it suffices, for now, to know that we have long been fabricating economic “growth” by allowing the stock of credit, and therefore of money, to drastically out-grow any meaningful measure of the flow of value within the economy.

Together, the scale and complexity of the bloated credit system mean that – probably at some esoterically-technical level – something is going to break, forcing the central banks into trying to prop up the system by flooding the economy with money.

But we can’t “print” our way to monetary stability, any more than we can borrow our way to prosperity.

This, unfortunately, is going to have to be learned the hard way.

6

« en: Hoy a las 11:09:57 »

Para mi lo estúpido es no dar la posibilidad que sea una mezcla entre lo humano y lo natural. Es decir, ¿8000 millones de personas arramplando con todos los recursos naturales, contaminación de todo tipo vertida al medio y miles de millones de máquinas, no han contribuido en nada a que el clima cambie?. Pregunto.

Así es, y tan estúpidos como los que lo achacan al factor antropogénico

7

« en: Ayer a las 11:21:02 »

https://crashoil.blogspot.com/2024/05/chispazo.htmlhttps://www.eleconomista.es/energia/noticias/12829605/05/24/espana-estuvo-anoche-al-borde-de-un-gran-apagon.html

Lo único raro que pasó ayer fue una parada no programada de Ascó (creo que de úno de los dos reactores).

El artículo empieza como queriendo echarle la culpa a la eólica y a la hidráulica.

El problema es que el suelo nuclear te lo están dando 7 reactores de los cuales dos (Vandellós y Trillo) están parados por diferentes razones, así que te quedas con 5. Si en esta situación uno se para, pierdes el 20% de la producción nuclear.

Igual el riesgo se asumió al programar las paradas de Vandellós y Trillo a la vez. Sin tener ni idea, igual se hizo así porque normalmente la primavera es buena en eólica e hidráulica y durante las horas de día tienes la fotovoltaica a todo meter. Pero entonces sucedió un cúmulo de catastróficas desdichas, se para de emergencia uno de los reactores que quedan en una noche de poco viento.

8

« en: Mayo 24, 2024, 20:30:44 pm »

Ppcc acertó en su día , hubo bajadas de entre el 40 y 60%. Lo que esperábamos, en general pienso yo, es que lo que pasó no iba a volver a pasar. Pero se ha decidido otra cosa, bienvenido Mr. Feudalismo. Creo que los bbcc han tenido mucho que ver o, más bien, quienes controlan los bbcc. En cualquier caso habrá reversión a la media, y cuanto más se estire la estupidez, más hostión habrá, como tantas otras veces. ¡Es el ser humano, amigos! https://en.wikipedia.org/wiki/Extraordinary_Popular_Delusions_and_the_Madness_of_CrowdsDigamos que el ladrillo vale cuesta infinito, bueno, pues después vendrá la energía, luego vendrá la sanidad, luego la educación, luego la alimentación, luego el agua y finalmente, se inventarán algo para acaparar oxígeno en botellitas, y si no puedes pagarlas...es el mercado amigos. Tal y como está montado, sólo puede quedar uno. Añado lo siguiente sobre el comportamiento irracional.

CONFUSION DE CONFUSIONES

JOSE DE LA VEGA

Sinopsis de CONFUSION DE CONFUSIONES

José de la Vega, publicó Confusión de Confusiones en Ámsterdam en 1688. Considerado el primer libro sobre la bolsa y objeto de estudio de los historiadores de la economía, Confusión de confusiones proporciona importantes datos sobre la vida bursátil y la actividad financiera de los judíos de Ámsterdam en el siglo XVII. Pero el interés de esta obra no se agota ahí: de su lectura se desprende que no estamos tanto ante la obra de un economista cuanto ante unas memorias sobre la bolsa, que recogen la experiencia directa del autor en al catástrofe de la Compañía de Indias y el descalabro de la Bolsa de Ámsterdam en 1688, vivencias y hechos presentados en forma de miscelánea dialogada, mediante la que Vega nos muestra su erudición literaria y filosófica.

9

« en: Mayo 24, 2024, 12:37:51 pm »

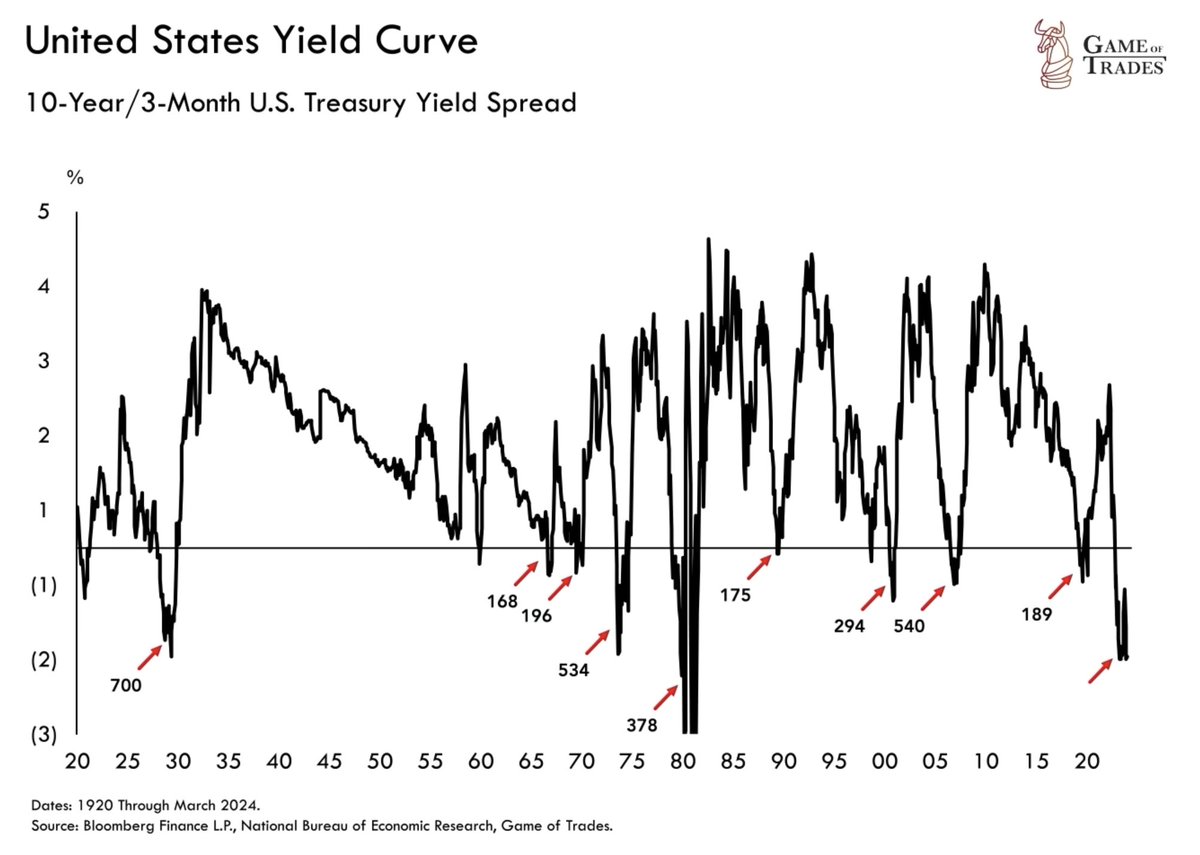

Hostión y muerte por aplastamiento, buena apreciación. Yo tampoco querría bajar tipos. Game of Trades

@GameofTrades_

·

22 may.

The yield curve has been inverted for almost 600 days now

This has only happened ONCE since 1920 → In 1929

Which ended up in the Great Depression and big market decline

We expect a final rally to occur before recessionary concerns finally kick in later in 2024

10

« en: Mayo 23, 2024, 17:26:26 pm »

11

« en: Mayo 22, 2024, 15:07:06 pm »

La que se está jodiendo es España, esa sí que está jodida. Manda huevos que se justifique o defienda al terraplanista que te insulta en tu propia tierra, ¿dónde están los patriotas? (¡hasta el punto de llamarle drogadicto!) No he leído o escuchado que se le haya llamado drogadicto, sólo he escuchado algo sobre "ingesta de sustancias". Igual era una bebida energética o mucho café.

12

« en: Mayo 21, 2024, 00:55:21 am »

No lo se, igual nos puedes iluminar. O como he comentado alguna que otra vez, es simple estupidez mezclada con complejidad. Pero vamos, poderes económicos y militares siempre han existido, ¿verdad?. Veo a las élites asustadísimas, por cierto.

13

« en: Mayo 20, 2024, 22:34:50 pm »

Puede ser que no lo sean, o sí. Un lavado de cara y listo.

https://es.wikipedia.org/wiki/Agrupaci%C3%B3n_Nacional_(Francia)

La Agrupación Nacional —en francés: Rassemblement national, RN, denominado hasta 2018 como Frente Nacional (FN) (en francés: Front national)— es un partido político francés considerado por los especialistas como de extrema derecha,15n. 1aunque se declare de derecha23 moderada.

Sus orígenes se encuentran en una coalición de partidos de la extrema derecha francesa, cuando fue fundado en octubre de 1972 y presidido desde ese momento hasta enero de 2011 por Jean-Marie Le Pen. A partir de entonces fue sustituido por su hija Marine Le Pen,24 que encabezó un proyecto de mejoramiento de la imagen del partido (desdemonización).25 Su nombre completo, en su creación, era Front National pour l'Unité Française (Frente Nacional para la Unidad Francesa).

https://es.wikipedia.org/wiki/Vox_(partido_pol%C3%ADtico)

Vox («voz» en latín)35n. 3n. 4 es un partido político español de ideología ultraconservadora54 y ultranacionalista78910 fundado el 17 de diciembre de 2013. Vox está calificado por especialistasn. 5 como un partido de ultraderecha,n. 6 de derecha radical populistan. 7 o de extrema derecha.n. 8n. 2 Sin embargo, algunos medios de tendencia conservadora prefieren referirse al partido como de derecha.n. 1 El presidente del partido es Santiago Abascal, su vicepresidente y secretario general es Ignacio Garriga.82

A nivel de la Unión Europea, Vox es miembro del Partido de los Conservadores y Reformistas Europeos (ECR), un grupo parlamentario europeo menos radical que el ultraderechista83 Identidad y Democracia (ID), en el que Vox declinó la invitación a integrarse.84

Entonces IU, Podemos o Sumar, son izquierda moderada. Y la CUP también.

Pues ayer en Vistalegre hubo una reunión que indica lo contrario. Estoy de acuerdo que el auge de estos individuos es una consecuencia, pero extrema derecha (o como la quieras llamar) haberla, hayla. Ya ha pasado otras veces, sigo recomendando el libro End Times de Peter Turchin.

Esas élites que están nerviosas porque no hay sitio para todos, o porque algunos dentro de ellas, pueden perder sus puestos de privilegio.

¿Entonces damos por bueno que VOX or Milei son extrema derecha? Lo digo porque en los pocos vídeos y muchos tweets que he visto del evento no vi exhibición de ningún tipo de fascismo ni nada que me hiciera tener miedo si perteneciera a un colectivo tradicionalmente objetivo de grupos fascistas.

Utilizamos el término "extrema derecha" con una facilidad alarmante. A mí que he visto en primera persona lo que de verdad es la extrema derecha, decir que Abascal es fascista/nazi o como lo quieran llamar, me da la risa.

Si en España de verdad hubiera 3 millones de fascistas (número de votantes de VOX), hace tiempo que habría estallado una guerra civil con muchos muertos. Ni siquiera me hacen falta 3, con que hubiera 1 millón hace mucho que se habría liado un follón sin retorno.

Es que curiosamente es la izquierda la que decide quién es izquierda y quién derecha, y hemos llegado a un punto en que cualquier cosa a la derecha del PSOE es extremaderecha. ¿O no se acuerdan cuando a Rivera le llamaban Falangito?

La izquierda se ha refundado tantísimas veces que ya no defiende a los obreros, ahora defiende a las minorías, pero sólo a algunas y algunas son mejores que otras (por eso las masas se lanzan a la calle a defender a las mujeres -menuda minoría, el 50% de la población-, a no ser que el agresor sea inmigrante. Entonces no.)

Yo soy socialista convencido. Creo en un Estado con servicios públicos de calidad gratuitos o semigratuitos para todos, financiados con unos impuestos justos y proporcionales. No estoy en contra de la educación o la sanidad privada, siempre que no sean un sustituto de la pública.

Que wikipedia diga que VOX es extrema derecha a mí no me dice nada. ¿Se han leído el programa? Díganme en qué punto ven una política de extrema derecha. No vayan a lo que dicen otros, vayan a lo que ellos mismos proponen y díganme cuáles de sus puntos son de extrema derecha y por qué.

Los que son de extrema derecha de verdad no lo ocultan ni lo tratan de disimular, lo exhiben orgullosos, igual que los comunistas no pierden ocasión de restregarte por la cara la estrella o la hoz y el martillo.

A ver, que en las manifestaciones de Ferraz había banderas con pollo, sin pollo o directamente con un agujero, y también mucho putodefender a España y tal. Al final estos partidos salen por la inacción de los que deberían haber hecho las cosas de otra manera, pero como estos no mandan y son marionetas, pues, potato, poteito, tomato, tomeito. Me da lo mismo que lo llames extrema derecha o extrema estupidez. Son un síntoma, o como muy bien dices, una consecuencia. Y luego cada uno tenemos nuestras fobias y sesgos,y a mi lo de poner una terraplanista como ministra de ciencia me ha revuelto. De ahí a quemar libros o prohibirlos porque no son "libertarios" y hablan de cosas extrañas que "mi, no entender"...

A ver, los que hemos tenido (y tenemos) que aguantar a los fatxas del Arrano Beltza y sus Presoak ka(ga)lera, amnistia osoa, y los ongi etorris, nos partimos el culo con las paridas de que si los "fachas"de Vista Alegre o Milei y su motosierra.

Aquí (en este sitio concreto que todos ya sabéis) amigos, si te ibas de la lengua o si te emborrachabas y desvelabas tu verdadero pensamiento lo tenías (y tienes) chungo no, lo siguiente.

Ahora esos Fatxas son de izquierda de toalavida y progres pero progres patanegra porque me lo ha dicho el chulo de Tetuan...

Claro que sí guapis!

Vamos que esto es un no parar de reir....

Efectivamente, es lo que produce lo cómico y lo circense. https://www.elespanol.com/opinion/20240519/milei-mezclar-libertad-carajo-portarse-persona-non-grata/856544348_13.html

14

« en: Mayo 20, 2024, 20:06:55 pm »

15

« en: Mayo 20, 2024, 18:20:22 pm »

Puede ser que no lo sean, o sí. Un lavado de cara y listo.

https://es.wikipedia.org/wiki/Agrupaci%C3%B3n_Nacional_(Francia)

La Agrupación Nacional —en francés: Rassemblement national, RN, denominado hasta 2018 como Frente Nacional (FN) (en francés: Front national)— es un partido político francés considerado por los especialistas como de extrema derecha,15n. 1aunque se declare de derecha23 moderada.

Sus orígenes se encuentran en una coalición de partidos de la extrema derecha francesa, cuando fue fundado en octubre de 1972 y presidido desde ese momento hasta enero de 2011 por Jean-Marie Le Pen. A partir de entonces fue sustituido por su hija Marine Le Pen,24 que encabezó un proyecto de mejoramiento de la imagen del partido (desdemonización).25 Su nombre completo, en su creación, era Front National pour l'Unité Française (Frente Nacional para la Unidad Francesa).

https://es.wikipedia.org/wiki/Vox_(partido_pol%C3%ADtico)

Vox («voz» en latín)35n. 3n. 4 es un partido político español de ideología ultraconservadora54 y ultranacionalista78910 fundado el 17 de diciembre de 2013. Vox está calificado por especialistasn. 5 como un partido de ultraderecha,n. 6 de derecha radical populistan. 7 o de extrema derecha.n. 8n. 2 Sin embargo, algunos medios de tendencia conservadora prefieren referirse al partido como de derecha.n. 1 El presidente del partido es Santiago Abascal, su vicepresidente y secretario general es Ignacio Garriga.82

A nivel de la Unión Europea, Vox es miembro del Partido de los Conservadores y Reformistas Europeos (ECR), un grupo parlamentario europeo menos radical que el ultraderechista83 Identidad y Democracia (ID), en el que Vox declinó la invitación a integrarse.84

Entonces IU, Podemos o Sumar, son izquierda moderada. Y la CUP también.

Pues ayer en Vistalegre hubo una reunión que indica lo contrario. Estoy de acuerdo que el auge de estos individuos es una consecuencia, pero extrema derecha (o como la quieras llamar) haberla, hayla. Ya ha pasado otras veces, sigo recomendando el libro End Times de Peter Turchin.

Esas élites que están nerviosas porque no hay sitio para todos, o porque algunos dentro de ellas, pueden perder sus puestos de privilegio.

¿Entonces damos por bueno que VOX or Milei son extrema derecha? Lo digo porque en los pocos vídeos y muchos tweets que he visto del evento no vi exhibición de ningún tipo de fascismo ni nada que me hiciera tener miedo si perteneciera a un colectivo tradicionalmente objetivo de grupos fascistas.

Utilizamos el término "extrema derecha" con una facilidad alarmante. A mí que he visto en primera persona lo que de verdad es la extrema derecha, decir que Abascal es fascista/nazi o como lo quieran llamar, me da la risa.

Si en España de verdad hubiera 3 millones de fascistas (número de votantes de VOX), hace tiempo que habría estallado una guerra civil con muchos muertos. Ni siquiera me hacen falta 3, con que hubiera 1 millón hace mucho que se habría liado un follón sin retorno.

Es que curiosamente es la izquierda la que decide quién es izquierda y quién derecha, y hemos llegado a un punto en que cualquier cosa a la derecha del PSOE es extremaderecha. ¿O no se acuerdan cuando a Rivera le llamaban Falangito?

La izquierda se ha refundado tantísimas veces que ya no defiende a los obreros, ahora defiende a las minorías, pero sólo a algunas y algunas son mejores que otras (por eso las masas se lanzan a la calle a defender a las mujeres -menuda minoría, el 50% de la población-, a no ser que el agresor sea inmigrante. Entonces no.)

Yo soy socialista convencido. Creo en un Estado con servicios públicos de calidad gratuitos o semigratuitos para todos, financiados con unos impuestos justos y proporcionales. No estoy en contra de la educación o la sanidad privada, siempre que no sean un sustituto de la pública.

Que wikipedia diga que VOX es extrema derecha a mí no me dice nada. ¿Se han leído el programa? Díganme en qué punto ven una política de extrema derecha. No vayan a lo que dicen otros, vayan a lo que ellos mismos proponen y díganme cuáles de sus puntos son de extrema derecha y por qué.

Los que son de extrema derecha de verdad no lo ocultan ni lo tratan de disimular, lo exhiben orgullosos, igual que los comunistas no pierden ocasión de restregarte por la cara la estrella o la hoz y el martillo.

A ver, que en las manifestaciones de Ferraz había banderas con pollo, sin pollo o directamente con un agujero, y también mucho putodefender a España y tal. Al final estos partidos salen por la inacción de los que deberían haber hecho las cosas de otra manera, pero como estos no mandan y son marionetas, pues, potato, poteito, tomato, tomeito. Me da lo mismo que lo llames extrema derecha o extrema estupidez. Son un síntoma, o como muy bien dices, una consecuencia. Y luego cada uno tenemos nuestras fobias y sesgos,y a mi lo de poner una terraplanista como ministra de ciencia me ha revuelto. De ahí a quemar libros o prohibirlos porque no son "libertarios" y hablan de cosas extrañas que "mi, no entender"...

|